Table Of Content

In most cases, shortening your loan term allows you to pay off your principal faster. A shorter term often means you'll have a higher monthly payment but fewer overall payments, reducing interest over the life of your loan. Additionally, shorter-term loans (i.e. 15-year fixed) typically have lower interest rates than those with longer terms (i.e. 30-year fixed). Mortgage payments are amortized, meaning your mortgage total remains the same each month, but the amount of principal and interest varies with each payment.

How Much Does It Cost To Refinance A Mortgage?

“Expert verified” means that our Financial Review Board thoroughly evaluated the article for accuracy and clarity. The Review Board comprises a panel of financial experts whose objective is to ensure that our content is always objective and balanced. Similar to getting a purchase mortgage, refinancing requires you to file an application, go through the underwriting process and close. Let’s consider some important initial aspects of refinancing a mortgage — and then run through the process step by step. You might want to refinance your existing mortgage for a variety of reasons. Just like when you bought your home, you must get a refinance appraisal before you refinance.

Types of mortgage refinance

It’s a good idea to use a mortgage refinance calculator to figure out your break-even point after accounting for refinancing expenses. For 30-year fixed refinances, the average rate is currently at 7.33%, an increase of 3 basis points over this time last week. When the slider shifts from red to orange, it means that the interest savings total more than the closing costs during that period — but your monthly payments will be higher. This usually happens when you shorten the loan term, say from 30 years to 15 years. Refinancing your mortgage means replacing an existing home loan with a new one.

Rocket Mortgage

Some financial institutions offer discounts to existing customers; you might also find military discounts. Finally, the lower your loan-to-value (LTV) ratio is, the lower your interest rate will be. If you don’t have to take cash out of your home when you refinance, you might want to avoid doing so as that will bump up your LTV and likely result in a higher interest rate. If you find any errors on your credit report, be sure to report them to both the credit bureau and the business that made the error as soon as possible. Both parties must correct the information in order for it to change on your credit report and be reflected in your credit score. The slider starts in the red, indicating that the closing costs exceed the interest savings at first.

You have the green light to refinance if both the payment and interest over time will go down. Speaking of green, the slider and the bars above it are green in this scenario (after a short segment of red). You can use equity tapped during a refinance to pay off debt, make home improvements or take action on whatever is your highest priority right now. Refinance rates are based on both factors you can control, like your personal finances, and some you can’t, like the market environment.

If something happens and you need to get out of your refinance, you can exercise your right of rescission to cancel any time before the 3-day grace period ends. Once underwriting and the home appraisal are complete, it’s time to close your loan. A few days before closing, your lender will send you a document called a Closing Disclosure. The exact length of time it’ll take to refinance your home can vary, but you can typically expect around 30 – 45 days. You can ensure that your refinance goes smoothly by responding to any inquiries from your lender as soon as possible. Your lender might ask for additional documentation supporting your employment or financial history during underwriting.

How to Refinance a Mortgage - CNET

How to Refinance a Mortgage.

Posted: Wed, 06 Mar 2024 08:00:00 GMT [source]

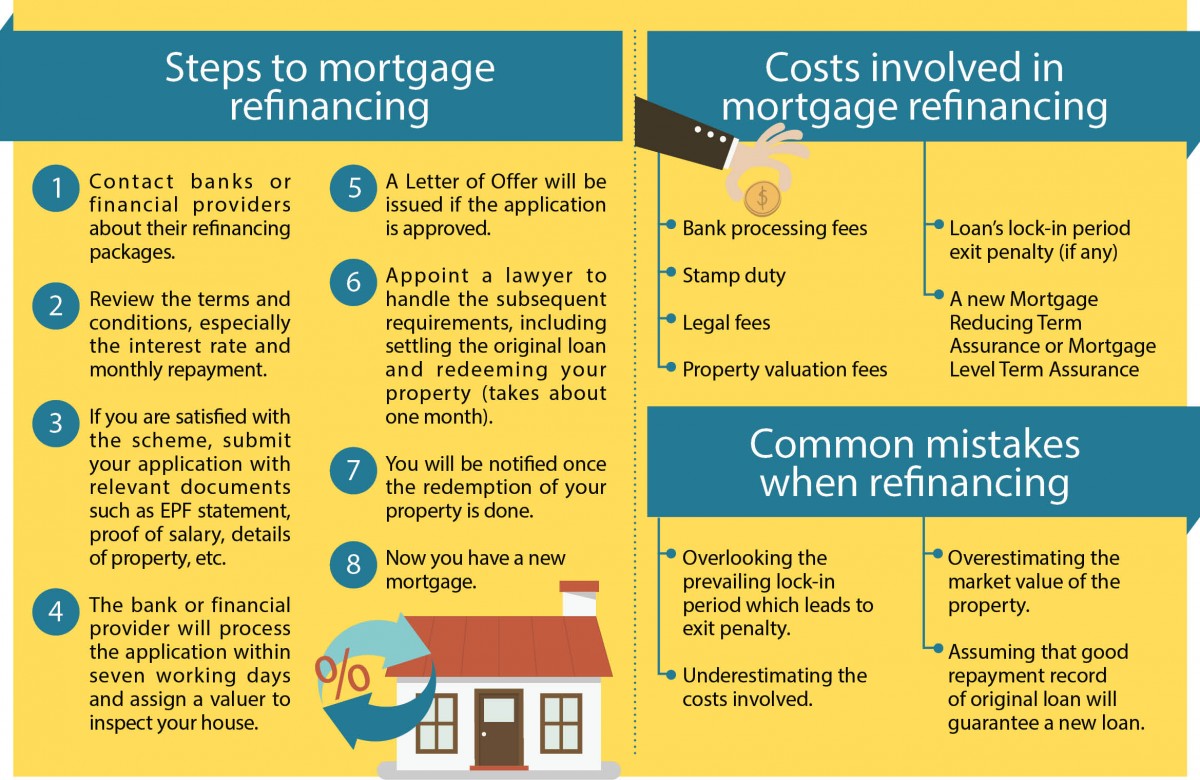

Refinancing a mortgage, step by step

Borrowers may also be able to avoid additional home appraisals or inspections on their property during the refinance process. Keep in mind that a cash-out refinance doesn’t add a monthly payment to your plate. The larger loan replaces your current mortgage, and the monthly payment amount will be higher or lower depending on the new loan agreement.

How Much Mortgage Can I Afford?

There is no minimum period set by conventional lenders for a rate-and-term refinance after you close. FHA and VA refinance programs require that you’ve made at least seven payments (on time) to be eligible for a refinance. You may need to wait up to a year after your closing if you’re taking cash out. A rate-and-term refinance allows borrowers to change the interest rate and loan terms of an existing mortgage. This tends to be a beneficial option when refinance rates are lower, and a borrower can pursue more favorable terms with their lender.

What Does It Mean To Refinance A Mortgage?

But getting the right mortgage for your situation is also important. We focus first on understanding you and your goals, not just your finances. While refinancing could be a good choice in several cases, it isn’t the right move for everyone. Here are some pros and cons to consider to help you decide whether you should refinance your mortgage.

Your credit score is not part of your credit reports, although it is based on the information they contain. One or more of your credit card issuers may provide your credit score for free. Otherwise you can obtain free credit scores from a variety of other sources. Slightly, but the long-term benefits of refinancing your mortgage can far outweigh the temporary downside. In 2023, Walker & Dunlop’s Capital Markets group sourced capital for transactions totaling nearly $12 billion from non-Agency capital providers. This vast experience has made them a top adviser on all asset classes for many of the industry’s top developers, owners, and operators.

With this type of refinance, your lender replaces your existing mortgage with a loan that has a reduced balance. The monthly payments are lowered to a level you can realistically afford. So, you get to keep your property, and your lender loses less money than if the home had been foreclosed or gone through a short sale. Depending on your lender, you might have the option of a no-closing-cost refinance, which is where these fees are rolled into your total loan amount. However, while this means you might save some money on your closing day, you’ll likely end up with a slightly higher interest rate—and you’ll be paying interest on your closing costs. Bankrate.com is an independent, advertising-supported publisher and comparison service.

They’re great ways to pay for things like home improvements, tuition, big events and more. It’s possible to negotiate certain lender fees—such as getting them to waive the underwriting and processing fees. Fees imposed by the government as well as third-party expenses like taxes, attorney review fees and home appraisals can’t be negotiated or waived. Much of the slider and the bars below it may be red in this scenario, indicating that you'll pay more total interest and closing fees during that period. A typical refinance will cost between 2% and 6% of your loan amount, but there are different ways to pay the costs.

Bankrate has reviewed and partners with these lenders, and the two lenders shown first have the highest combined Bankrate Score and customer ratings. You can use the drop downs to explore beyond these lenders and find the best option for you. For example, if you have an adjustable-rate mortgage (ARM) and the rate is about to increase, you can change to a more stable fixed-rate mortgage. Monitor refinance rates regularly and use Zillow’s free refinance calculator to make sure a refinance is worth it for your financial circumstances.

No comments:

Post a Comment